Main Blog Article Content

6 MIN. READ

The South Florida housing market can be challenging to navigate. With limited inventory and rising prices, it is more important than ever to adopt a strategic approach to homeownership and choosing the right mortgage product.

Understanding the South Florida Housing Market

The South Florida housing market is characterized by rising prices and an insufficient inventory. In 2023, prices for single-family homes in Miami-Dade increased by 15% on average, while condo prices went up by 9%. Experts find the situation concerning and estimate that South Florida homes are overvalued by 36% on average. This trend will likely continue as South Florida communities like Sunny Isles Beach, Lauderhill, and Kendall have some of the fastest-growing home prices in the state.High prices create an advantageous market for sellers, but inventory can't keep up as Florida's population continues to grow. New construction also struggles to keep up. On average, projects take over a year to complete as construction companies face an ongoing labor shortage.

The situation could worsen as falling interest rates cause more buyers to enter the market. This could result in an even more competitive environment where many buyers have to settle for properties in need of extensive renovations, adding significant costs in an already expensive market.

Choosing the right South Florida mortgage product to finance your home is more important than ever. It will ensure that your monthly payments remain affordable even as prices continue to rise.

Comparing Different Types of South Florida Mortgage Products

There are different types of mortgages to consider:- Fixed-rate mortgages have an interest rate that remains the same for the entire term of the loan. You'll know exactly what your monthly payment will be, but qualification requirements can be strict.

- Adjustable-rate mortgages have a rate that changes at regular intervals. They're easier to qualify for, but payments can increase and be hard to predict.

- Federal Housing Administration (FHA) loans are an excellent option for first-time buyers. Not all properties are eligible, but you can benefit from a lower down payment and a more affordable rate.

- As a veteran, you can qualify for a Veteran Affairs (VA) loan with no down payment and a competitive rate.

- Due to rising home prices, more buyers are applying for jumbo mortgages. These non-conforming loans allow you to borrow more than the $766,550 per property limit set by the Federal Housing Finance Agency.

- Do you qualify for an FHA or VA loan? If yes, these products are likely the most affordable options.

- Will your home be a short-term or long-term investment? An adjustable-rate mortgage might sense if you plan to move in a few years.

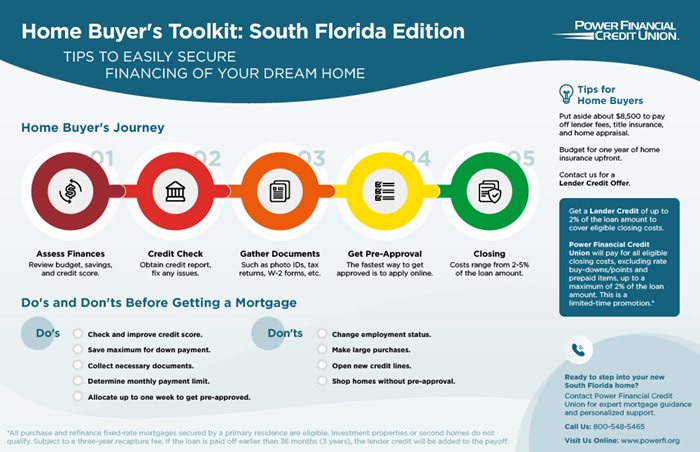

Pre-approval Process and Requirements

Getting pre-approved for a South Florida mortgage shows you're a serious buyer. As of July 2023, homes lasted only 45 days on the market before being purchased. Getting pre-approved allows you to act fast once you find your dream home.Here are the steps to getting pre-approved:

- Get your finances in order. Then, determine how much you have for your down payment and how much you want to get pre-approved for.

- Choose a mortgage provider and decide on the type of mortgage that works best for you.

- Fill out a pre-approval application. Most financial institutions will let you complete this step online.

- The lender will run a credit check, verify your income, and ensure you have enough to cover your down payment.

- Once the lender approves your application, you'll receive a pre-approval letter.

What to Do or Not Do Before Getting a Mortgage

Getting your finances in order before applying for a mortgage can improve your chances of qualifying for a lower rate.Do's:

- Get your credit report and look for ways to improve your credit score.

- Save for the largest down payment possible.

- Gather the necessary documents, including your income tax returns and proof of income.

- Go over your budget and determine how much you can afford to spend on your monthly mortgage payment.

- If you want to compare rates from different lenders, get all pre-approvals during the same week to have credit checks count as a single inquiry on your credit report.

Don'ts:

- Avoid any changes to your employment status.

- Don't make large purchases or open new credit lines.

- Don't start shopping for a home without getting pre-approved for a South Florida mortgage first and figuring out how much home you can afford.

Budgeting for Closing Costs

Closing costs are a significant expense that must be budgeted for. These costs can include:- An origination fee from your lender that typically won't exceed 1% of the loan. Some lenders will also charge processing and underwriting fees.

- You'll have to pay for a title search and title insurance policy.

- Your lender will require a home appraisal, and you'll likely want to pay for a comprehensive home and pest inspection.

- Expect additional fees if you want to buy points to lower your mortgage rate.

- Home insurance prices have been rising in Florida, with the average policy costing $6,000 a year. You'll likely have to pay for a year in advance at closing.

- The good news is that property tax rates are relatively low in Florida, with an average of 0.91%. Your closing cost will include property taxes for six months to a year in advance.

- Additional fees can include paying for mortgage insurance in advance, escrow fees, a commission for your real estate agent, HOA fees, flood determination and monitoring fees, and a property survey fee.

First-Time Homebuyer Programs and Resources

These programs can help you save on your home purchase:- FHA-backed loans are one of the most affordable options for first-time homebuyers.

- Find out more about VA-backed loans if you qualify as a veteran.

- The Florida Assist and Florida Homeownership Loan Programs available through Florida Housing allow you to borrow up to $10,000 as a second mortgage to cover your down payment.

- The Broward County's Homebuyer Purchase Assistance Program is an income-based program that lets you borrow funds to cover closing costs.

- If you're a teacher, law enforcement officer, first responder, firefighter, or other type of community worker, HUD's Good Neighbor Next Door Program and the Florida Hometown Heroes Housing Program can help you save on your home purchase.

Plan Your Home Purchase With Power Financial Credit Union

Power Financial Credit Union has been serving the South Florida community since 1951. Our mission is to make homeownership accessible with a variety of affordable and flexible mortgage products.Besides offering personalized mortgage advice and a wide rage of home loan products, we can help you cover eligible closing costs by offering a lender credit of up to 2% of the loan amount.

Get started by using our mortgage loan calculator to see how a mortgage payment would fit within your budget, or learn more about the types of mortgages we offer.

FAQs

Learn more about homeownership with these common questions.What impacts do hurricanes and flood zones have on costs?

Buying a home in a hurricane or flood zone will lead to stricter insurance requirements and higher insurance costs.

What documentation is required for self-employed individuals seeking a mortgage in South Florida?

Your lender will likely ask for your income and business tax returns and bank statements documenting your income.

Can you include multiple borrowers on a mortgage in Florida?

You can apply for a joint mortgage. Your lender will review your finances, credit score, and your co-applicant's profile. If your co-applicant has a strong profile, it can help your application.